OTTAWA

,

March 4, 2022

(press release)

–

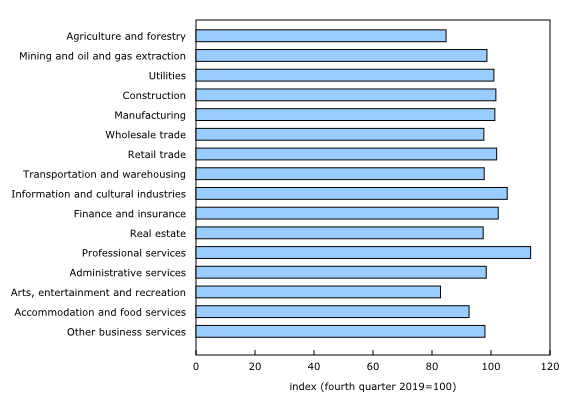

Productivity decreases again, but much less than in the previous five quarters Chart 1: Hours worked in Canadian businesses increase slightly faster than real output In the fourth quarter, productivity fell for the sixth consecutive quarter, following the record increase observed in the second quarter of 2020. Since the third quarter of 2020, hours worked have increased more or decreased less than the business output. Compared with the fourth quarter of 2019—the last quarter before the pandemic began—productivity was down 1.2% in the fourth quarter of 2021. The public health measures in place in the fourth quarter were essentially the same as in the third quarter, and were some of the least restrictive since the start of the pandemic. Despite the emergence of the Omicron variant and the implementation of new public health rules starting in mid-December, growth in business output continued in the fourth quarter, even outpacing that of the previous quarter. Meanwhile, hours worked continued to increase at a similar pace as in the third quarter and again surpassed output growth. Business output continues to grow at a higher rate than in the third quarter In the fourth quarter, the output of service-producing businesses had almost returned to its pre-pandemic level (-0.1% compared with the fourth quarter of 2019). However, output of goods-producing businesses has yet to catch up. Overall, all major industry sectors increased their output in the fourth quarter of 2021, except utilities (-0.1%). Hours worked increase at a similar pace as in the third quarter Chart 2: Comparison of changes in business output and hours worked In the fourth quarter, hours worked rose in both goods-producing businesses (+1.8%) and service-producing businesses (+2.9%). Hours worked in some sectors did not completely return to the levels seen in the fourth quarter of 2019, but differences between sectors did narrow. In total, 7 of the 16 industry sectors topped their pre-pandemic level. Chart 3: Changes in recovery of hours worked by industrial sector, fourth quarter 2021 The increase in hours worked in the fourth quarter was largely due to the 2.2% gain in employment, while hours worked per job edged up 0.4%. The number of people with more than one job rose 5.5%, after increasing 7.6% in the third quarter. Meanwhile, the number of people who were absent without pay was down 1.9%, after falling 14.2% in the third quarter. Losses in work hours in the business sector are similar to the third quarter At the industry level, the loss of work hours in the fourth quarter continued to affect most sectors and was also of similar magnitude as in the previous quarter. The sectors most affected by the loss of work hours in the fourth quarter were the same ones affected since the pandemic began: other business services, retail trade, accommodation and food services, construction, professional services, and manufacturing. These six sectors, which comprise businesses that cannot operate without physical proximity among people, accounted for nearly 70% of hours lost in the fourth quarter. Chart 4: Work hours lost in the fourth quarter 2021 because of COVID-19 pandemic, by industry, business sector For the second consecutive quarter, other business services continued to post the largest loss of all sectors, with a net loss of 8.2 million hours in the fourth quarter. This sector includes a variety of businesses, such as personal and laundry services (including hair salons and beauty salons) and repair and maintenance services, whose activities were in large part affected by public health measures. Service-producing businesses are the main source of the decline in productivity Overall, productivity was down in 10 of the 16 main industry sectors and was unchanged in construction. In the fourth quarter, accommodation and food services (-6.1%) and real estate services (-3.5%) posted strong declines in their productivity. By contrast, the largest increases in productivity were in arts, entertainment and recreation (+7.8%) and in agriculture and forestry (+7.4%). In the United States, the labour productivity of businesses rebounded 1.6% in the fourth quarter, after falling 1.2% in the previous quarter. This was the largest quarterly growth rate since the second quarter of 2020 (+2.5%). In the fourth quarter of 2021, real GDP growth of American businesses accelerated to 2.2% from 0.4% in the previous quarter, while the increase in hours worked slowed to 0.6% in the fourth quarter, after rising to 1.7% in the third quarter. Impacts of the COVID-19 pandemic on hours worked in the business sector, fourth quarter of 2021 Unit labour costs are almost the same level as in the third quarter The average value of the Canadian dollar relative to the US dollar did not fluctuate in the fourth quarter. As a result, unit labour costs of Canadian businesses expressed in US dollars (-0.1%) were practically unchanged, when compared with the costs not adjusted for the exchange rate. By comparison, unit labour costs of American businesses edged up 0.1%, with both productivity (+1.6%) and hourly compensation (+1.7%) posting similar gains. Annual averages for 2021 This historic drop in productivity comes after an all-time high of 8.1% in 2020, when GDP of businesses (-6.8%) and hours worked (-13.3%) posted record decreases. While 2020—the year the pandemic was declared—was characterized by stricter public health measures in most parts of the country, 2021 saw a net rebound in hours worked (+12.1%) and real GDP of businesses (+4.8%), thanks to high rates of vaccination against COVID-19 and further easing of public health restrictions. This was an unprecedented annual increase in hours worked and the largest increase in business output since 2000 (+6.1%). In the business sector, the net effect of the pandemic on hours worked was a loss of 377.2 million hours for all of 2021. This is a much smaller loss than in 2020 (-836.5 million hours). In the United States, productivity of businesses rose 1.9% in 2021. This annual gain was driven by an increase in the GDP of American businesses (+7.2%), while hours worked were up 5.2%. These are the biggest annual increases since 1984, when they rose 8.9% and 5.9%, respectively. In Canadian businesses, unit labour costs were up 4.5% in 2021, their largest annual increase since 1991 (+5.8%). In 2021, labour productivity of businesses (-6.9%) posted a greater decline than hourly compensation (-2.8%), which led to this annual increase in unit labour costs. When the annual average 7.0% appreciation of the Canadian dollar relative to the US dollar in 2021 is taken into account, the unit labour costs of Canadian businesses expressed in US dollars jumped 11.8%. This was the biggest annual growth rate since 2003 (+14.5%), when the Canadian dollar appreciated strongly (+12.4%). By comparison, unit labour costs of American businesses grew 3.4% in 2021. Note to readers Revisions Productivity measures Labour productivity is a measure of real GDP per hour worked. Unit labour cost is defined as the cost of workers' wages and benefits per unit of real GDP. The approach to measuring real output in the business sector differs from the one that is used in the estimates by industry. For the business sector, output is measured using the expenditure-based GDP approach at market prices. This approach is similar to that used for the quarterly measures of productivity in the United States. However, output by industry is based on the value added at basic prices. All the growth rates reported in this release are rounded to one decimal place. They are calculated with index numbers rounded to three decimal places, which are now available in data tables. All necessary basic variables for productivity analyses (such as hours worked, employment, output and compensation) are seasonally adjusted. For information on seasonal adjustment, see Seasonally adjusted data – Frequently asked questions. Next release Products The Latest Developments in the Canadian Economic Accounts (Catalogue number13-605-X) is available. The User Guide: Canadian System of Macroeconomic Accounts (Catalogue number13-606-G) is available. The Methodological Guide: Canadian System of Macroeconomic Accounts (Catalogue number13-607-X) is available. Contact information Industry Intelligence Editor's Note: This press release omits select charts and/or marketing language for editorial clarity. Click here to view the full report.

Labour productivity of Canadian businesses decreased 0.5% in the fourth quarter, while hours worked increased slightly more than business output. This was a smaller decline in productivity than in each of the previous five quarters.

Real gross domestic product (GDP) of businesses rose 2.0% in the fourth quarter, after increasing 1.4% in the previous quarter. As a result of this increase, output moved much closer to its pre-pandemic level (-1.1% compared with the fourth quarter of 2019).

Hours worked in the business sector rose 2.6% in the fourth quarter, a similar increase as in the previous quarter (+2.7%). With this increase, in the fourth quarter, hours worked were 0.1% above their pre-pandemic level.

When only workers who were active or on paid leave are taken into account, the net effect of COVID-19 on hours worked in the business sector was a loss of 55.9 million hours in the fourth quarter. This loss was comparable to the one in the third quarter (-57.3 million hours).

In the fourth quarter, the decline in productivity was mainly attributable to service-producing businesses, whose productivity fell 0.8%, following a similar decline in the previous quarter (-0.9%). In contrast, productivity of goods-producing businesses edged up 0.1%, after decreasing 1.2% in the third quarter.

Estimates of hours worked in the business sector are mainly based on data from the Labour Force Survey (LFS). It should be noted that for hours worked (used to measure productivity), both main and secondary jobs are considered—not only the main job as in the LFS. The main survey for the LFS for the reference period that includes the months of October, November and December does not capture losses of work hours outside the reference weeks. To account for those, as with the previous seven quarters, the estimates of hours lost because of the pandemic were adjusted using a compilation of supplementary questions added to the LFS questionnaire in November, December 2021 and January 2022 for the respective reference months of October, November and December 2021. These adjustments are reflected in the data on hours worked and related measures (including labour productivity) for the fourth quarter of 2021.

In Canadian businesses, both productivity (-0.5%) and average compensation per hour worked (-0.6%) decreased at a similar pace in the fourth quarter. As a result, labour costs per unit of output of Canadian businesses were stable (-0.1%) in the fourth quarter, after rising over the previous four quarters.

On average over the year 2021, labour productivity of Canadian businesses fell 6.9%, while hours worked rebounded much more than business output.

Volatile data starting in the first quarter of 2020

For two years now, quarter-to-quarter data have been particularly volatile, reflecting the impacts of the pandemic and health measures on economic activity and the labour market. Given the strong variations over the last eight quarters, the percentage changes from the pre-pandemic level—i.e., from the fourth quarter of 2019—can better reflect the changes in productivity and related measures than percentage changes from quarter to quarter. However, the quarterly data in Table 1 of this release are presented only in the usual format: the percentage change from the same quarter in the previous year and the change from the previous quarter.

With this release, data were revised back to the first quarter of 1997 at the aggregate and industry levels. These revisions are consistent with those incorporated in the annual benchmarks on provincial and territorial labour productivity and related measures, released on February 11, 2022. They are also consistent with those incorporated in the quarterly gross domestic product (GDP) by income and expenditure and monthly GDP by industry, released on March 1, 2022. In addition, indexes of all series at the aggregate level were subject to historical revision going back to 1981, as a result of revisions to the values for the 2012 reference year. However, the resulting revisions to growth rates were negligible.

The term productivity in this release refers to labour productivity. For the purposes of this analysis, labour productivity and related variables cover the business sector only.

Labour productivity, hourly compensation and unit labour cost data for the first quarter of 2022 will be released on June 3.

The Economic accounts statistics Portal, accessible from the Subjects module of our website, features an up-to-date portrait of national and provincial economies and their structures.

For more information, or to enquire about the concepts, methods or data quality of this release, contact us (toll-free 1-800-263-1136; 514-283-8300; infostats@statcan.gc.ca) or Media Relations (statcan.mediahotline-ligneinfomedias.statcan@statcan.gc.ca).

* All content is copyrighted by Industry Intelligence, or the original respective author or source. You may not recirculate, redistrubte or publish the analysis and presentation included in the service without Industry Intelligence's prior written consent. Please review our terms of use.