OTTAWA

,

June 14, 2022

(press release)

–

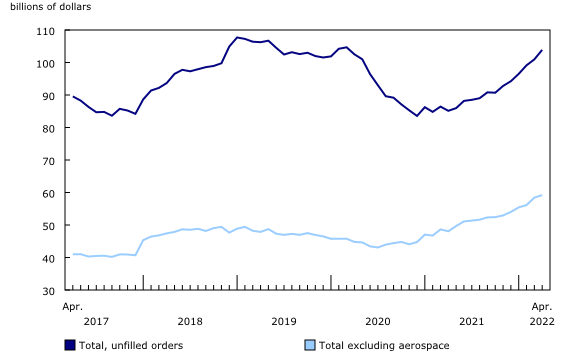

Manufacturing sales rose 1.7% to $72.3 billion in April, mainly on higher sales in the petroleum and coal product (+3.7%), motor vehicle (+8.2%), and primary metal (+4.1%) as well as higher production of aerospace product and parts (+11.2%) industries. Meanwhile, wood product sales decreased the most (-6.0%). Chart 1: Manufacturing sales Sales in constant dollars rose 0.9% in April, indicating that both prices and volume sold contributed to the gains in April. The Industrial Product Price Index rose 0.8% in April. Petroleum sales continue to increase Sales of motor vehicles increased 8.2% to $4.5 billion in April, the third month-over-month increase and the highest sales since August 2020. Year over year, sales in the motor vehicle industry were up 100.4%. Accordingly, sales of motor vehicle parts rose 2.0% to $2.7 billion. Exports of motor vehicles and parts rose 3.9% in April, the highest level since October 2020. Following an 8.6% increase in March, primary metal sales rose 4.1% to $6.2 billion in April, on higher prices and volumes sold. The limited metal production in China due to the COVID-19 pandemic and global supply interruptions due to the Russia aggression against Ukraine led to an increase in prices of basic and semi-finished iron or steel products (+3.2%). Monthly sales in constant dollars rose 2.9% in April, while year over year, sales were up 26.0%. Higher production of aerospace product and parts (+11.2%) and higher sales of food (+1.2%) and machinery (+3.0%) also contributed to the gains in the manufacturing sector in April. Following seven consecutive monthly increases, wood product sales declined 6.0% to $4.5 billion in April, primarily on lower prices. Prices for softwood lumber were down 13.7%, while exports of lumber and other sawmill products decreased 2.6% in April. Wood product sales in constant dollars were down 1.3%. Sales of paper products decreased 7.9% to $2.5 billion in April, following a 10.1% increase in March. Despite the decline in April, sales of paper products were up 4.1% compared with the same month a year earlier. Sales of paper in real terms fell 10.1% month over month in April. Sales also declined in the non-metallic mineral product (-3.8%), beverage and tobacco product (-3.4%) and other transportation equipment (-16.0%) industries in April. Sales in Alberta increase the most, mainly on higher petroleum sales In Alberta, sales rose 6.5% to $9.5 billion in April, primarily on higher sales of petroleum and coal products (+15.5%) and chemicals (+15.1%). The gains were partially offset by lower sales of fabricated metal products (-13.1%). On a year-over-year basis, total sales in Alberta rose 37.6% in April. In Quebec, sales increased 2.1% to $18.0 billion in April, the fourth consecutive month-over-month gain. The increase was mainly attributable to sales of primary metals (+8.2%) and production of aerospace product and parts (+27.6%). With the increase in April, total manufacturing sales in Quebec were up 20.0% year over year. In British Columbia, following seven consecutive monthly increases, sales declined 2.9% to $5.8 billion in April, mainly on lower sales in the paper and wood product industries. Despite the decrease in April, total sales in British Columbia stood 7.3% higher compared with the same month a year earlier. Edmonton marks the largest increase in sales among selected census metropolitan areas Sales in Edmonton were up 12.2% to $4.9 billion in April, mainly on higher sales of petroleum products (+19.1%). The petroleum and coal product industry has been the main contributor to manufacturing sales in Edmonton since February 2022. Year over year, total sales in Edmonton rose 70.3% in April. Sales in Montréal increased 3.9% to $7.9 billion in April, on higher sales in 10 of 21 industries. The gains were driven by higher production of aerospace product and parts (+72.8%) and sales of machinery (+21.5%) and computer and electronic products (+4.3%). Sales in Québec fell 8.0% to $2.0 billion in April, following a 16.9% increase in March. Lower sales of petroleum and coal products were almost entirely responsible for the decline. Despite the decrease, total sales in Québec were up 58.8% year over year in April. Record-high inventory levels continue Chart 2: Inventory levels rise The inventory-to-sales ratio increased from 1.54 in March to 1.55 in April. This ratio measures the time, in months, that would be required to exhaust inventories if sales were to remain at their current level. Chart 3: The inventory-to-sales ratio increases Unfilled orders rise Chart 4: Unfilled orders rise The total value of new orders marked a new record high, rising 3.1% to $75.2 billion in April mainly on higher new orders of aerospace product and parts, fabricated metals and motor vehicles. Capacity utilization rate declines on lower production Chart 5: The capacity utilization rate decreases The capacity utilization rates fell in 17 of 21 industries in April and were most noticeable in the transportation equipment (-2.7 percentage points), petroleum and coal product (-3.7 percentage points), machinery (-2.7 percentage points) and computer and electronic product (-6.0 percentage points) industries. The declines were partially offset by a higher production capacity rate in the non-metallic mineral product industry (+2.4 percentage points). Note to readers Seasonally adjusted data are data that have been modified to eliminate the effect of seasonal and calendar influences to allow for more meaningful comparisons of economic conditions from period to period. For more information on seasonal adjustment, see Seasonally adjusted data – Frequently asked questions. Trend-cycle estimates are included in selected charts as a complement to the seasonally adjusted series. These data represent a smoothed version of the seasonally adjusted time series and provide information on longer-term movements, including changes in direction underlying the series. For information on trend-cycle data, see Trend-cycle estimates – Frequently asked questions. Both seasonally adjusted data and trend-cycle estimates are subject to revision as additional observations become available. These revisions could be large and could even lead to a reversal of movement, especially for reference months near the end of the series or during periods of economic disruption. Non-durable goods industries include food; beverage and tobacco products; textile mills; textile product mills; clothing; leather and allied products; paper; printing and related support activities; petroleum and coal products; chemicals; and plastics and rubber products. Durable goods industries include wood products; non-metallic mineral products; primary metals; fabricated metal products; machinery, computer and electronic products; electrical equipment; appliances and components; transportation equipment; furniture and related products; and miscellaneous manufacturing. Production-based industries For the aerospace and shipbuilding industries, the value of production is used instead of the value of sales of goods manufactured. The value of production is calculated by adjusting monthly sales of goods manufactured by the monthly change in inventories of goods in process and finished products manufactured. The value of production is used because of the extended period of time that it normally takes to manufacture products in these industries. Unfilled orders are a stock of orders that will contribute to future sales, assuming that the orders are not cancelled. New orders are those received, whether sold in the current month or not. New orders are measured as the sum of sales for the current month plus the change in unfilled orders from the previous month to the current month. Manufacturers reporting sales, inventories and unfilled orders in US dollars Some Canadian manufacturers report sales, inventories and unfilled orders in US dollars. These data are then converted to Canadian dollars as part of the data production cycle. For sales, based on the assumption that they occur throughout the month, the average monthly exchange rate for the reference month established by the Bank of Canada is used for the conversion. The monthly average exchange rate is available in table 33-10-0163-01. Inventories and unfilled orders are reported at the end of the reference period. For most respondents, the daily average exchange rate on the last working day of the month is used for the conversion of these variables. However, some manufacturers choose to report their data as of a day other than the last working day of the month. In these instances, the daily average exchange rate on the day selected by the respondent is used. Note that because of exchange rate fluctuations, the daily average exchange rate on the day selected by the respondent can differ from both the exchange rate on the last working day of the month and the monthly average exchange rate. Daily average exchange rate data are available in table 33-10-0036-01. Revision policy Each month, the Monthly Survey of Manufacturing releases preliminary data for the reference month and revised data for the previous three months. Revisions are made to reflect new information provided by respondents and updates to administrative data. Once a year, a revision project is undertaken to revise multiple years of data. Real-time data tables Real-time data tables 16-10-0118-01, 16-10-0119-01, 16-10-0014-01 and 16-10-0015-01 will be updated on June 22, 2022. Next release Data from the Monthly Survey of Manufacturing for May will be released on July 14, 2022. Contact information Industry Intelligence Editor's Note: This press release omits select charts and/or marketing language for editorial clarity. Click here to view the full report.

Sales of petroleum and coal products marked a new record high, rising 3.7% to $10.1 billion in April, the fourth consecutive monthly gain. Higher prices were mainly responsible for the increase as real value sales increased 0.5%. The global disruptions of energy supply caused by the Russian invasion of Ukraine were responsible for the surge in prices of refined petroleum energy products (including liquid fuels), which increased 4.7% in April. Exports of refined petroleum energy products were up 14.4% in April.

Manufacturing sales increased in six provinces in April, led by Alberta and Quebec. British Columbia posted the largest decline.

Manufacturing sales increased in 7 of the 15 census metropolitan areas in April, led by Edmonton and Montréal. Sales in Québec declined the most.

Total inventory levels increased 2.3% to $111.8 billion in April, mainly on higher inventories of the machinery (+5.6%), chemical (+3.8%) and miscellaneous manufacturing (+12.6%) industries. Meanwhile, inventories of motor vehicles declined 10.0% in April.

The total value of unfilled orders rose 2.9% to $103.9 billion in April, the sixth consecutive monthly increase and the highest level since March 2020. The gains were mainly attributable to higher unfilled orders in the aerospace product and parts (+5.0%), fabricated metal (5.9%), and machinery (+3.9%) industries. The total value of unfilled orders rose 22.0% on a year-over-year basis in April.

The capacity utilization rate (not seasonally adjusted) for the total manufacturing sector decreased from 81.9% in March to 79.9% in April on lower production.

Monthly data in this release are seasonally adjusted and are expressed in current dollars, unless otherwise specified.

For more information, or to enquire about the concepts, methods or data quality of this release, contact us (toll-free 1-800-263-1136; 514-283-8300; infostats@statcan.gc.ca) or Media Relations (statcan.mediahotline-ligneinfomedias.statcan@statcan.gc.ca).

* All content is copyrighted by Industry Intelligence, or the original respective author or source. You may not recirculate, redistrubte or publish the analysis and presentation included in the service without Industry Intelligence's prior written consent. Please review our terms of use.